The rise of Arini

Fast growing hedge fund and credit platform

Money that chases star traders is not a new trend. But what makes Arini interesting is that it goes against the grain of recent multi-strategy and pod shop dominance of the industry. Hamza Lemssouguer – a trader with zero pure buy-side experience – has in only three and a half years created a $9-10bn credit investing platform. It reminds me of the golden age before the Volcker rule when star traders from banks - mostly from the proprietary trading desks - would launch large new hedge funds.

Lemssouguer almost joined Citadel five years ago but the way Arini is performing, it is unlikely that he has been having any regrets. One can imagine that Ken Griffin reminds his head of credit and co-CIO Pablo Salame that parrot whisperer Lemssouguer (he owns a parrot farm and is an avid parrot conservationist) was the one who got away!

The origin story of Arini

In a short span of six years’ Hamza Lemssouguer went from Credit Suisse graduate trainee to not just head of European high-yield trading but one of the biggest individual revenue generators in the firm. Lemssouguer would make big bets on blocks of distressed corporate debt, often dominating the flows in those securities.

In early 2020 IFR estimated that Hamza made $120m of the $140m of trading profits the desk had made in 2019. In 2021 Bloomberg estimated that his desk made $220m in 2020 and wrote that competitors had complained after being outplayed. Bloomberg said that marketing materials prepared by Credit Suisse asset management showed that, “During his time at Credit Suisse, Moroccan-born Lemssouguer generated a gross annualized return of 38%, including 81% in 2019 and 44% in 2020.”

Dan Davies discussed how Credit Suisse asset management had changed its mind about supporting Lemssouguer’s hedge fund launch in efinancialcareers back in early 2021. When Credit Suisse started imploding, Lemssouguer was forced to look elsewhere and found backing from Squarepoint, a fast-growing quant hedge fund also run by École Polytechnique graduates. I wrote about Squarepoint in The French Connection.

Returns and growth

Since launching at the start of 2022, Lemssouguer’s Arni has performed in the same style that the team did while at Credit Suisse – high returns but with high volatility. It is built around the high convictions of its CIO and founder Lemssouguer. But in interviews he has given he tries to stress the amount of time that the Arini team spends on portfolio construction, on how to play themes in a way that ensures asymmetric risk profiles and overall risk management. Lemssouguer says that Arini tries to match its long and short positions over time to ensure that it is not overly exposed directionally. Nevertheless, the nature of taking large bets on illiquid European corporate distressed debt is that volatility in returns is a feature rather than a bug of Arini’s business model.

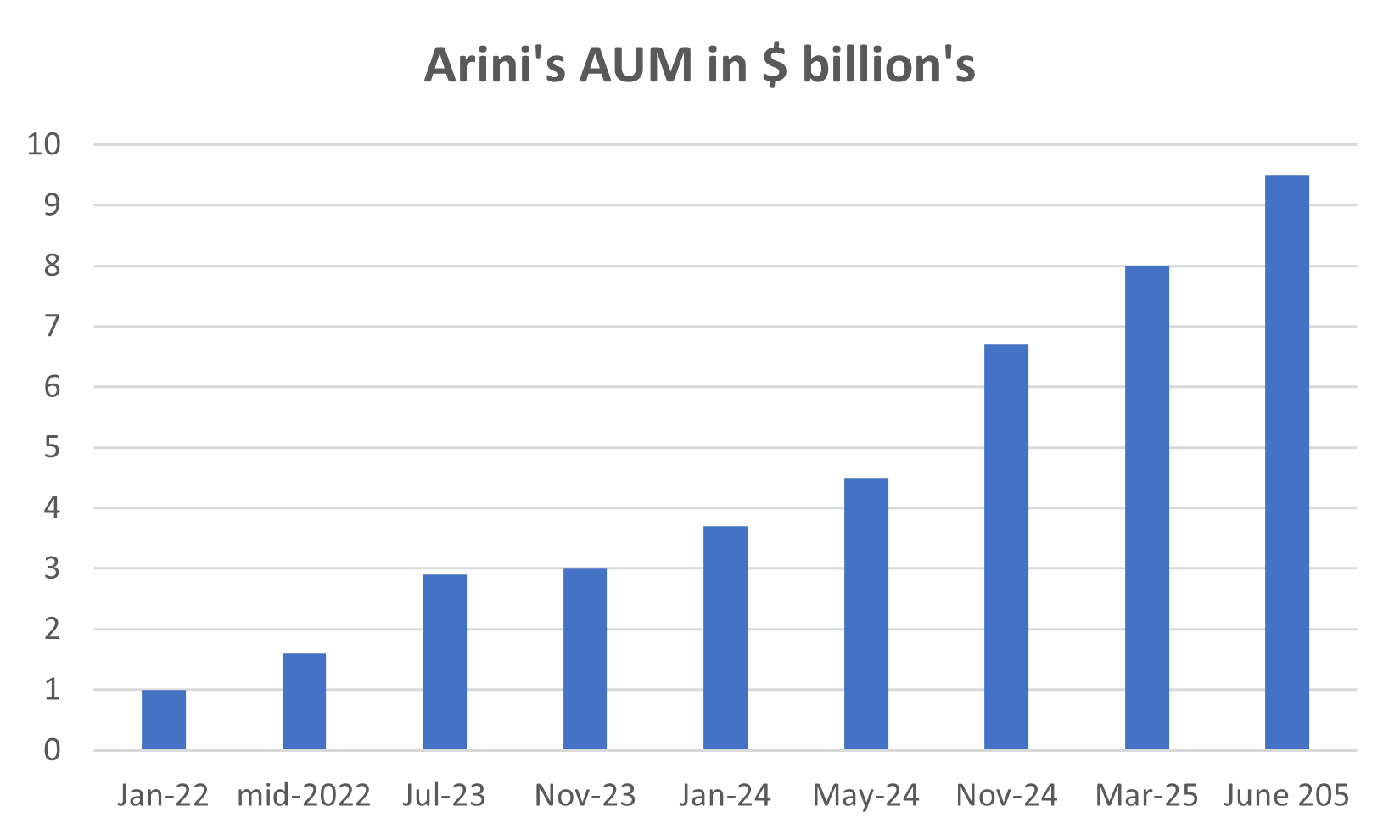

Arini’s start was a baptism of fire in terms of the pressure on credit markets caused by Russia’s invasion of Ukraine in early 2022. After struggling for most of the year in tough credit markets, Arini recovered and posted a very respectable 4% net return for 2022. This was followed by stellar returns of 25.8% in 2023, 22.2% in 2024, and 10% plus in the first half of 2025. Arini has consistently outperformed most other credit hedge funds by a wide margin since its launch.

Fund flows followed in both the Master Fund and across other funds, making Arini the fastest-growing new European hedge fund launch in recent years. Risk-averse institutional allocators have been chasing established multi-strategy hedge funds. But in Lemssouguer they believe they have found a new superstar of the industry. They may be right.

Where new hedge funds have raised substantial money from external fund allocations by multi-strategy hedge funds, this is typically in segregated managed accounts (SMAs). Arini’s fund-raising for its master fund of $1bn at launch and further fund-raising for this fund in the following year or two were all in the same fund structure rather than segregated managed accounts. In addition to operational support, it received seed capital from Squarepoint at launch but there has been a diverse set of institutional allocators to this Master Fund since then. This contrasts with other big launches. Taula Capital, founded last year by Diego Megia received $3bn of its initial $5bn from Megia’s former employer Millennium.

A diversified credit platform

The core of Arini is bottom-up fundamental analysis. It has one of the largest dedicated European high-yield credit research teams, with many of them following their CIO Hamza Lemssouguer from Credit Suisse. As AUM and the number of funds have expanded fast so has the Arini team, which is now around 90, a more than fourfold increase over the last two years.

Just over half of Arini’s current AUM of around $9-10bn is in its Master Fund that trades credit long/short. The latter’s fund performance was of course important for not just fund-raising here but also other Arini funds. With the Master Fund largely closed to new money now, there has been an increasing amount of AUM going into other Arini funds in the last year. Hamza Lemssouguer has said from the start that his ambition was broader than merely trading high-yield bonds to offer a broad credit platform that was agnostic about the distinction between public and private markets.

In mid-2022 Arini hired BNP Paribas European head of ABS and CLO trading Mehdi Kashani to build out a CLO platform leveraging Arini’s large research team and new hires with CLO and structured credit expertise. In November 2023 Arini’s first European CLO raised €401m. This was followed by 3 more European CLO launches in the following twelve months raising a further a further €1.7bn. By the time Arini closed fund-raising for its first-ever US CLO in April 2025, it had raised a total of $2.5bn for its CLO platform. Of course, the economics of this business are very different relative to that of a hedge fund but it is scalable, and a steady revenue source.

As well as the master fund and CLOs, Arini has always offered co-investment opportunities for its clients. Several other funds such as the structured credit equity fund and a recent credit opportunities fund together raised a billion dollars. Moreover, like many public market credit investors, Arini has moved into private credit. British Columbia Investment Management anchored this fund with $250m. Arini has said that it has one billion dollars of capital to deploy in private credit, once including leverage. A year ago, Arini hired former Credit Suisse investment banking co-head Mathew Cestar to help build its relationships with corporate borrowers and private equity. It has also recently announced a partnership with investment bank Lazard which will help Arini source EMEA SME private credit opportunities. A few weeks ago, Arini announced that it is opening an Abu Dhabi office.

New multi-PM fund

Earlier this week With Intelligence reported that “Arini is working on plans to launch a multi-PM fund” and “that Arini plans to debut the fund in the second half of 2025.” The fund will trade more than a dozen sub-categories of credit with the existing team of portfolio managers, each managing separate parts of the fund, with limited overlap. But this new fund will not charge pass-through fees.

This comes at a time when we are finally seeing some fund-raising activity in terms of new hedge funds outside the multi-strategy world. With Intelligence also reported that two former Deutsche Bank distressed credit veterans - Gavin Colquhoun and Rahul Ahuja (ex-Fortress) – are working on the launch of a London-based European distressed credit hedge fund.

Through the cycle

The Arini team did well both on the short and long side during the turbulence of 2020 and 2022 so it is unfair to say that they are bull market investors. But it will be interesting to see how they would perform in a sustained credit crunch where there wasn’t a sharp V-shaped cycle and Federal Reserve bailout.

Almost 20 years ago I worked on the IPO of what was the Arini of its day, a credit manager called BlueBay. At the time BlueBay had $8bn of assets under management in credit funds. BlueBay had a great structural story of the emergence of active European bond managers. It also had a great investment team that had put up several years of stellar returns across all of its funds. But the majority of BlueBay’s earnings came from its long/short hedge funds, in particular its distressed debt hedge fund. When the Global Financial Crisis hit BlueBay’s high-yield hedge fund suffered extremely badly given rising defaults, the illiquidity of positions, and redemptions. It never fully recovered. In periods of continued market dislocation - as I found out in covering bank’s stocks during the GFC - sometimes even a “hedged” book can have massive losses as liquidity drives mismatches between longs and shorts or basis risk blows out.

Despite Arini’s amazing returns in recent years, Lemssouguer has been vocal about his view that credit spreads have been too tight and that with most European high-yield duration being relatively short-term, there is a wall of refinancing coming with many companies likely to struggle. He believes that having deep-domain knowledge in not just the specific credits and industries but also the country-specific legal and bankruptcy code is a key point of differentiation for Arini versus smaller or less focused investment teams.

In recent years top pod shops have extended the time it takes their investors to fully redeem their funds, from one year to four years or longer. There is very little publicly known about Arini’s asset base but given the nature of the investments it makes it would be surprising if Arini didn’t use its strong start to ensure that has more long-duration capital locked in.

Fast forward

Arini’s is expanding fast in headcount, AUM, and fund structures. But Lemssouguer believes that bottom-up fundamental credit analysis is its DNA so don’t expect it to follow the industry trend and diversify into other areas whether it is macro, equities, or anywhere else.

The European distressed debt markets have always been small relative to the US markets with Europe more the home of macro and fixed-income relative value geniuses like Alan Howard, Chris Rokos, Mike Platt, and Yan Huo but things are changing. There has been significant growth in both European high-yield bonds and leveraged loans in recent years. Time will tell if Arini can navigate successfully the next credit crisis!