Starling and Revolut are from different worlds

Disparity between UK neobank's grows

“In a bull market, these FinTechs get sold to me as technology companies; in a bear market, I get rich shorting them as financial companies”

One of the areas I write about regularly is proprietary trading firms and more than once I have written “Two firms that were once direct peers — Jane Street and Flow Traders — are now as far apart as Amazon and Poundland.” A decade ago several fintechs started to compete head-to-head in the UK but recent trends show that Revolut and Starling are now as far apart as Amazon and Poundland!

Starling results lag peer group

Starling just reported results for the year ending March 2025 and they were not pretty and illustrate the challenge fintechs face.

I discussed the sector a few months ago: Are neobank's really tech or banking? Can banks compete with fintech? but what these results illustrate (we await Monzo in a few days, which should be better) is the rapid divergence in performance over recent years between the group of neobanks launched around 10 years ago.

Starling’s revenue growth of 5% was broadly in line with the 4% growth last year at OakNorth but materially lagged Revolut which grew by more than 70% for the calendar year 2024. Underlying revenue growth was even worse though at Starling at almost zero growth if we exclude a £25 million swing in fair value adjustment from the prior year. The chart below excludes that noise but either way after many years of robust revenue growth, Starling’s growth has stalled.

An even worse trend can be seen in profitability. Whereas OakNorth grew net income by 15%, Starling saw a decline of more than 30%. Excluding the fine for lax anti-money laundering (AML) controls and the impairment related to failure to follow UK government guidelines on the Covid-19 bounceback loans, Starling’s profits were still down though by 7%. This contrasted with 130% profit growth at Revolut. Starling’s staff costs grew by 32% year on year driven by 21% headcount growth.

But here’s the thing. It was not just the headline financial numbers but the underlying trends and the future risks that make you wonder how on earth Starling thought it was in IPO shape when it started looking for a head of Investor Relations last year.

Let’s start with customer growth. Starling is a one-country firm. Customer numbers of 4.6 million grew by 10% over the year, with no growth in the SME segment. By stark contrast, Revolut has added 12 million customers in each of the last two years, mostly through rapid international expansion but also growth in the U.K. Monzo has added 2 million UK customers in the last 6 months to reach a total of 12 million and Revolut has seen similar growth in the U.K. adding several million customers and reaching a similar total UK customer base to Monzo.

Whereas customer numbers can be a more VC tech metric, an operating metric that all bankers look at is deposit growth. Together with the number of products used, it illustrates customer penetration. A 10% increase in Starling’s deposit base to £12.1 billion over the last financial year contrasted with deposit growth of 65% at Revolut, 33% at OakNorth, and around 20%+ at Chase UK. (JP Morgan Chase had the added issue that it was coming near to the UK threshold of a maximum of £25 billion of deposits before consumer bank subsidiaries need ring-fencing. The U.K. government has recently announced this threshold will be revised to £35 billion.)

Crucially Starling’s deposit growth was driven exclusively by inflows into higher interest-paying savings accounts. Deposits into retail current accounts and SME accounts were down marginally over the period. Consequently, the biggest drag behind the decline in net interest margin from 4.34% to 4.12% was a £40m increase in these interest costs. Although interest rates started to fall during the period it had a limited impact during this financial year. Even in the prior year (year ending March 2024) when Starling had seen explosive net interest income growth of 70% this was virtually all driven by rising interest rates with customer numbers only growing 16% and its deposit growing by a mere 4%.

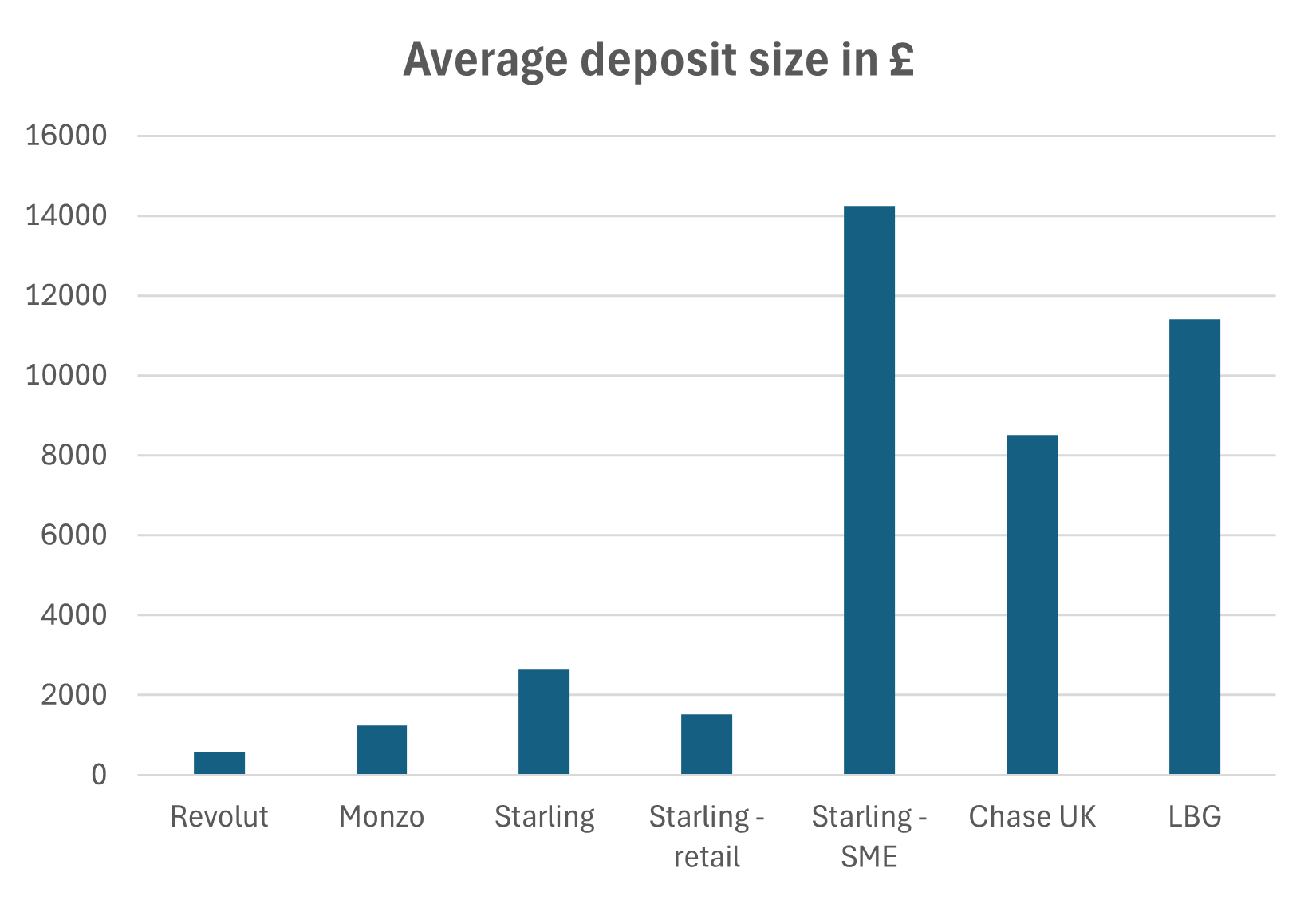

The chart below illustrates how Starling has a higher average deposit size than Revolut and Monzo but for retail customers’ it is broadly similar to Monzo and significantly below Chase UK and Lloyd’s Banking Group. Moreover, as the numbers earlier illustrated this is not growing and unlike Revolut it is not being held back by rapid onboarding of new customers.

From the other side of the balance sheet, Starling generated £812m of gross interest income, mostly from investments. As well as parking money at the Bank of England and buying Gilts, Starling appears to have moved up the risk spectrum and had tepid loan growth. Financials Unshackled by John Cronin provides a great summary of this.

Growth has historically differentiated fintechs from banks but as I have discussed before for a consistently high public market valuation, quality of earnings will matter and this means diversification beyond highly cyclical net interest income. Starling’s card transaction revenue i.e. interchange fees barely changed year over year with a decline from its SME business. This contrasts with Revolut, which generated £2.2 billion of non-interest income revenues in 2024, an increase of £1 billion in just one year from card interchange, crypto trading, stocks, FX, subscriptions, and other sources. Revolut also has huge geographical diversification with the UK only contributing 25% of its group revenues. In the year ending March 2024, Starling also saw relatively mediocre growth of 14% in its very small fee income from cards and interchange.

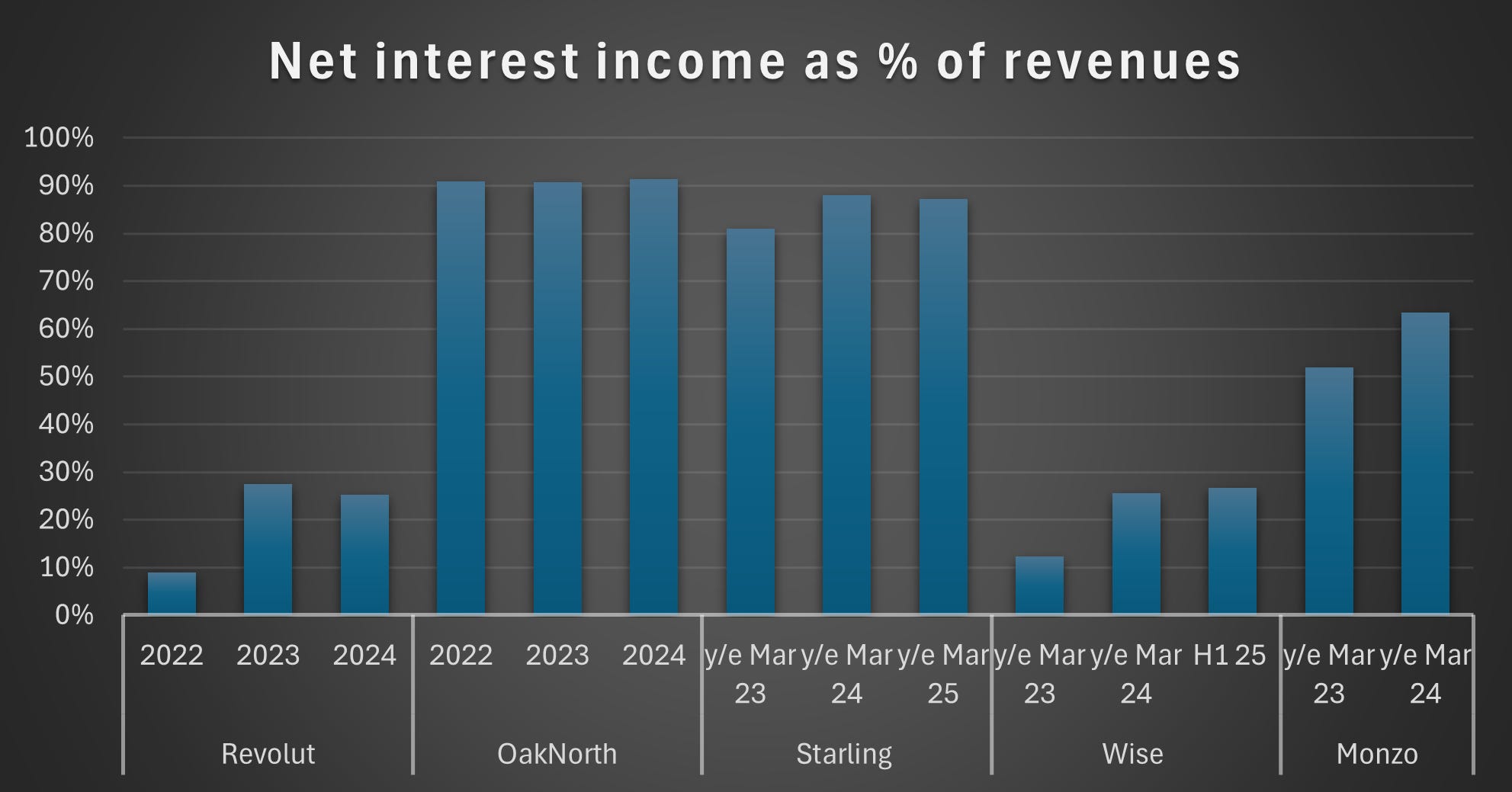

The chart below illustrates how Starling is much more dependent on net interest income than the likes of Revolut and even Monzo.

Starling generated a return on equity of 18% in 2024 (24.7% excluding impairment and fine), which was down on the 32% the prior year. This is still extremely healthy and in line with the average for the UK banking sector of 18% with only giants like Chase in the US and HSBC in global retail banking more in the 30% range out of Western banks.

Starling’s customer service and controls

One of Starling’s competitive advantages was strong brand recognition and customer service in its core UK market but it has faced increased competition in the space. In the annual Ipsos (FCA-mandated) survey of UK retail banking a few months ago, Starling fell to third behind Chase UK and Monzo. It will be interesting to see how Revolut does when it is included given its new UK banking license.

Improving controls and risk management is necessary for all of the neobanks that handle payments, loans, and deposits and hence will over time face regulation more like traditional banks than the tech startup world of moving fast and breaking thinking. Monzo CEO TS Anil recently highlighted that one of the largest challenges when Anil had become CEO was not product debt or tech debt but “controls debt” something very important for Monzo to get right if it wanted to scale with a wide product offering as a highly regulated institution.

For Starling, more worrying than the magnitude of the fine it paid for lax AML checks was how harshly it was rebuked by the FCA last year for these compliance failures: “Starling’s financial sanction screening controls were shockingly lax. It left the financial system wide open to criminals and those subject to sanctions. It compounded this by failing to properly comply with FCA requirements it had agreed to, which were put in place to lower the risk of Starling facilitating financial crime.” Starling found in 2023 that for the prior 6 years, its automated screening system for individuals on the sanction list had only been checking against part of the list!

Starling also has further risk management challenges with its loan book. This is currently heavily focused on buy-to-let property borrowers that are economically sensitive. Moreover, there may still be risks from the remaining Covid-19 era bounceback loans. It said in its results that it “may be exposed to further risks resulting in non-compliance with the eligibility requirements” that could affect its ability to claim under the guarantee contract or “retain payments already claimed under the guarantee contract”.

Starling the tech company

When Starling abandoned its geographical expansion plans a few years ago it said its focus was on selling its banking tech platform “Engine” to other banks. Out of the neobanks, only OakNorth was following a similar strategy. “Engine” would be a more comprehensive “Banking as a service” product than legacy vendors in the core banking space such as FIS, Temenos, and Finastra, or the newer cloud-native vendors like Mambu, Thought Machine, and 10x Technologies. Valuations of the latter had all soared in the 2021-2022 boom years including $5.3bn (30x revenue) for Mambu and $2.7bn (40x revenues) for Thought Machine. Starling shareholders thought that “Engine” would drive Starling’s valuation to £10bn Starling investor targets £10bn valuation for digital lender

But the banking tech platform business has proved to be tough. Incumbent legacy vendors are sticky and difficult to displace. Even the new cloud-native vendors have seen their revenue growth slow, gross margins struggle and cash burn levels remain very high.

So far, the number of clients and revenues for “Engine” has been negligible. Starling’s management team was extremely bullish but the only live clients are Salt, a Romanian digital bank, and AMP in Australia. In its results this week Starling finally outlined revenues for “Engine”, which were a mere £8.7m.

The bumpy road ahead

Starling’s challenge for the future is simple - where will growth come from?

The tech platform “Engine” neither has the customer pipeline from what has been announced to date nor the revenue trajectory to be a game changer.

A geographical buildout can be costly and time-consuming in terms of marketing spend, boots on the ground, and banking licenses. The European markets are also saturated with neobank expansions. Revolut has reached 3-4 million customers across each major Continental European market, German challenger N26 (after many years of restrictions on its growth tied to lax AML controls) saw 40% revenue growth in 2024 and has fresh capital, the Dutch firm Bunq has hit 17 million users across Europe and saw a 65% increase in 2024 profits, Monzo is launching its Continental European operations this year and Chase is planning to launch in Germany soon.

Starling has excess capital and is nicely profitable so there is no financial requirement to IPO beyond long-time shareholders looking to exit. At its last fund-raising round it raised £131m in April 2022 valuing Starling at £2.5bn. The business has grown considerably since then and sector valuations have risen. Using this valuation and dividing it by last year’s underlying net income gives a low double-digit price-to-earning multiple, undemanding for a fintech but still relatively high for a bank.

The future of Starling relies on its ability to re-accelerate deposit and customer growth in the UK. Despite some interest rate hedges in place, there will still be a substantial headwind from falling interest rates in the coming years so Starling needs to see 30-40% not a pedestrian 5-10% customer and deposit growth here. There may be lessons it can learn from Chase UK’s success with cashback offers and savings accounts or Monzo’s with financial planning tools. Otherwise, M&A increasingly looks like the only exit for Starling!

Brilliant analysis. I've seen many concepts similar to the B2B move Starling is making with Engine. "We've built something unique for B2C, the engine works well, but the market is very competitive, so let's sell it the engine to other businesses".

It always looks good on paper... but I've rarely seen it working (Blackrock's Aladdin?).

Combined with another concept that always sounds good but never takes off "we are going to replace the core banking" = A tough spot for Starling

...although they don't need to conquer the world.

Superb teardown. If UK PLC is gonna get its big boy growth pants 🩲 on, then it’ll need real banks that actually lend to real businesses (other than buy to let)

But I never hear about UK banks trying to improve either client risk mgt (KYC) or credit risk mgt…