Moving beyond Fixed Income

Where are macro funds and CTAs making money?

Everyone is focused on who has been making money and taking risk on the AI trade. After all, it has eaten the whole financial market. But this is not the only trend. Hedge funds are now having a great year like 2025, but the Soc. Gen. Trend Indicator shows wide divergences in momentum across asset classes. Moreover, in recent months the systematic CTAs have finally started to outshine discretionary macro hedge funds.

In this piece I look at:

the reversal of fortunes between discretionary and more systematic macro and trend-following strategies,

how the asset class dispersion is greater than the dispersion between discretionary and systematic (macro or trend-followers),

and who are the macro managers that are winning and who is bulking up in commodities and equities.

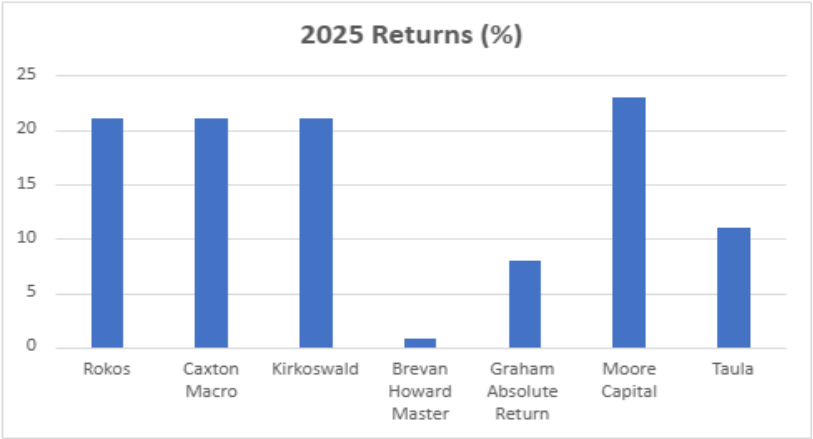

2025 and 2026 returns

In 2025, global macro hedge fund investment returns lagged equity long/short managers that had the tailwind of the bull markets in stocks.

Increased macro divergence, path dependence of interest rates, and cross-asset opportunities were a solid backdrop for most macro managers. Goldman Sachs noted that they were seeing increased allocator demand for discretionary macro.

Nevertheless, it was a tale of two cities. According to HFR, discretionary macro hedge funds were up 15-17% while systematic macro hedge funds were flat for the year. The chart below shows 2025 returns for some of the largest discretionary macro hedge funds.

Similarly, managed futures trend-following hedge funds also struggled in the first half of 2025 and were broadly flat for the year. The Soc. Gen. Trend indicator, which creates hypothetical returns across asset classes, found that trend-following should have generated a 2025 investment return of around 7% gross and 4% net of fees. But the Soc. Gen’s CTA Index of 20 actual systematic funds was flat, and the Soc. Gen Trend Index of 10 large pure trend-followers was up 2.4%. This followed very poor returns in the prior two years.

There has been a reversal of fortunes in 2026. Both macro systematic and discretionary hedge funds were up around 5% in January and did well in February. The systematic CTA/trend-following index also had a strong start to the year. According to HFR Index macro 2026 net returns as of the end of May of 7.5% made it the second-best performing strategy of the year. Discretionary macro was hit worse in the March volatility, and its year-to-date returns of under 7% are trailing the nearly 10% returns for systematic directional strategies. The Soc. Gen. CTA Index and the Soc. Gen. Trend Index are both up 10% this year.

All about commodities and equities for trend-followers

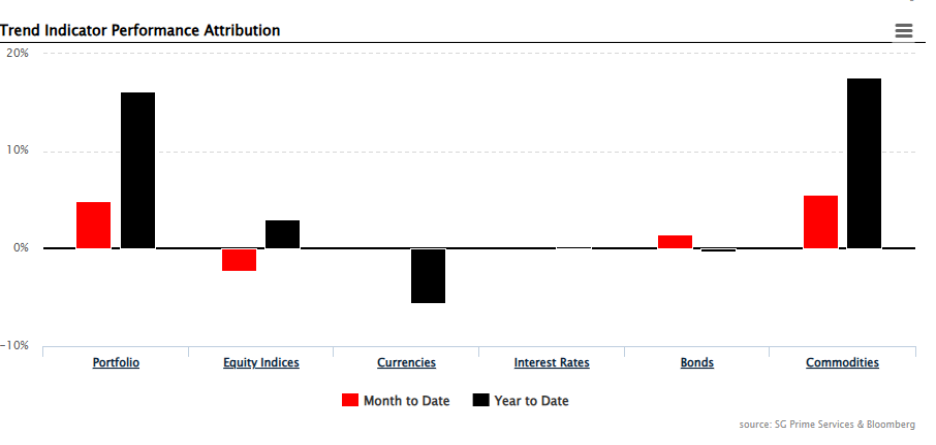

The Soc. Gen. Trend Indicator uses 55 futures contracts across a variety of asset classes. It then uses a simple 20-day/120-day moving average crossover to determine position direction. Although a replication and not 100% correlated to actual systematic CTA or trend-follower hedge fund returns, it gives good colour to the drivers behind trend-follower performance.

As of 10th June 2026, the Soc. Gen’s Trend Indicator is up around 16% on a gross basis and 13.5% net of fees. The chart below shows the former and the performance attribution from each asset class to the total. The key driver for outperformance has been commodities with equities making a smaller than expected positive contribution. By contrast, the struggles across traditional fixed income have continued, and currency trading has been particularly tough this year.

Strength in commodities was wide based. Half of this year’s performance is driven by gold and silver, but other winners include heating oil, RBOB, Crude oil, Coffee, and Cocoa. This contrasts with 2025 when Gold and Silver had made huge gains while energy and agricultural contracts had made losses.

2025 equity index returns for the trend-following indicator were steady and spread across numerous Continental European and Asian indexes. In 2026 equity indexes were again a positive contributor but almost completely dependent on the AI play that is South Korea’s KOSPI Index.

Both 2025 and 2026 have been tough for FI Macro across bonds and currencies. This follows a poor performance for trend-followers here in 2023 and 2024. The replication index suggests that in 2026 trend-followers are likely to have seen losses across the major European pairs, the New Zealand and Canadian dollars.

SG Trend Indicator Daily Report

A similar but less pronounced asset class trend can be seen across macro hedge funds. The HFR Macro Commodity Index was up 4.5% as of the end of May 2026. This is well below that of the Soc. Gen commodities trend indicators at the end of May 2026. The HRX Macro Active Trading Index performed well at 6.7% but again lagging trend-followers. Meanwhile, the HFR Macro: Currency Index was down 2% this year. It is the only one of the macro sub-indexes down albeit it isn’t as weak as the Soc. Gen FX trend indicators.

Multi-strategy giants struggle in FIC

Graham founder Ken Tropin told the FT that its discretionary PMs had made most of their 2025 returns trading the dollar, gold and US Treasuries. The precious metals trade has of course been hugely profitable for most large macro hedge funds through both 2025 and 2026. But many macro funds have struggled in traditional fixed income and foreign exchange markets.

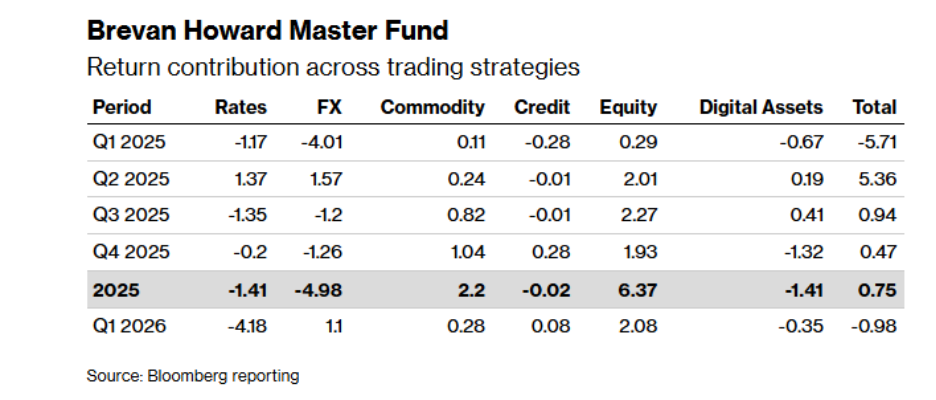

Brevan Howard is one of the oldest and most storied names in fixed income macro hedge funds. Alan Howard famously never had a down year in his decade plus as an investment bank proprietary trader and navigated the GFC well. Howard runs very little money directly nowadays, and earlier last year I wrote about Brevan Howard’s investment performance struggles and its inability to compete with the big US multimanager platforms. Things haven’t improved since then.

Bloomberg recently reported that “the number of US stocks and exchange-traded funds held by Brevan Howard funds has more than doubled to nearly 2,000 since the end of 2024...the total market value of such bets has risen to about $9 billion as of the end of March, from $2.4 billion in December 2024.”

It also noted that equities and to a lesser extent commodities - two traditionally small areas for the firm – had driven most investment returns in 2025 and Q1 2026. Meanwhile, Brevan Howard took heavy losses in FX and rates trading, which have been its core competency over the years.

Bloomberg attributed the equities’ returns to one of Brevan’s star multi-asset managers but also noted that the firm has recently been building a team of equity sector specialists to filter trade ideas to Brevan’s multi-asset portfolio managers. With Intelligence had previously reported that Brevan was setting up an external allocation programme targeted towards long/short equity.

Brevan Howard is not the only major macro fund to expand in equities. Howard’s former partner Chris Rokos has been putting up industry leading returns for years and has done well in equity indexes and commodities. It has been hiring equity long/short PMs. With Intelligence reported late last year that Graham had hired a former Millennium equities PM and Taula was also hiring equities managers as it looked to diversify beyond its traditional FI background. Greg Coffey’s Kirkoswald, which focuses on EM macro, has also made much of its gains in equities and commodities.