As expected UK fintech Monzo delivered strong results. TS Anil - the TradFi career banker who put on a hoodie recently for boy-wonder venture capitalist Harry Stebbings' podcast has not only stabilized the ship, he has driven huge successes. If you compare it to Starling which I discussed last week, Monzo has crushed it. Revenue growth in the last financial year at Monzo of 40-50% compared to low single-digit growth at Starling and OakNorth and only behind Revolut, which had 70% revenue growth last year. Monzo added 2.2m retail and 200,000 business customers in the last year, an overall growth rate in customer numbers of 25%. And customers left more with Monzo than before so deposits grew at an even faster 48%. These are impressive figures by any means.

Fintech neobank’s often get criticised for being nice shiny products but not the primary bank account for their customers, which could limit the amount of money they can make from each customer. Monzo says it is now the primary bank for one-third of its customers.

No wonder the company is starting to make noises that it is ready for an IPO. But the stock market is a forward-looking (albeit imperfect and prone to hype cycles and busts) mechanism. Shareholders will want to know what is the growth, moat, and economics of this business 5 years from now.

Despite its staggering growth in the last two years, Revolut has many risks around whether customers ever treat it as a primary bank, the cyclicality of some earnings streams like crypto, and whether it will drop the ball on risk and compliance. But Nik Storonsky has iterated fast in terms of geographical and product expansion and provided a clear vision of a technology and product backbone that will support creating the first truly global consumer bank more efficiently than any incumbent. Whether he can be fully successful or not is still to be proven and I have doubts about banks claiming to be superapps but at least I know what I am buying with Revolut and its lofty valuation.

Which brings me back to Monzo. Peter Thiel always says go very deep and become entrenched in a small vertical and then expand outwards. The question is always when do you expand? For instance, Amazon.com moved quickly horizontally beyond books into new categories and then started laying the seeds for vertical integration into logistics and AWS.

When I have spoken to Monzo management about their Achilles’ heel relative to Revolut of having a limited geographical footprint, they have argued that Monzo is stronger in the UK market than others and that their moat here continues to get deeper. After all Revolut’s global revenues may be three times larger but in the UK Monzo generates more revenue.

Monzo’s colorful cards, customer-friendly UI, and tools like budgeting have proved to be popular and the company has been consistently highly rated for its service quality in the annual Ipsos (FCA-mandated) survey of UK retail banking. So let’s dig a bit into Monzo’s UK business.

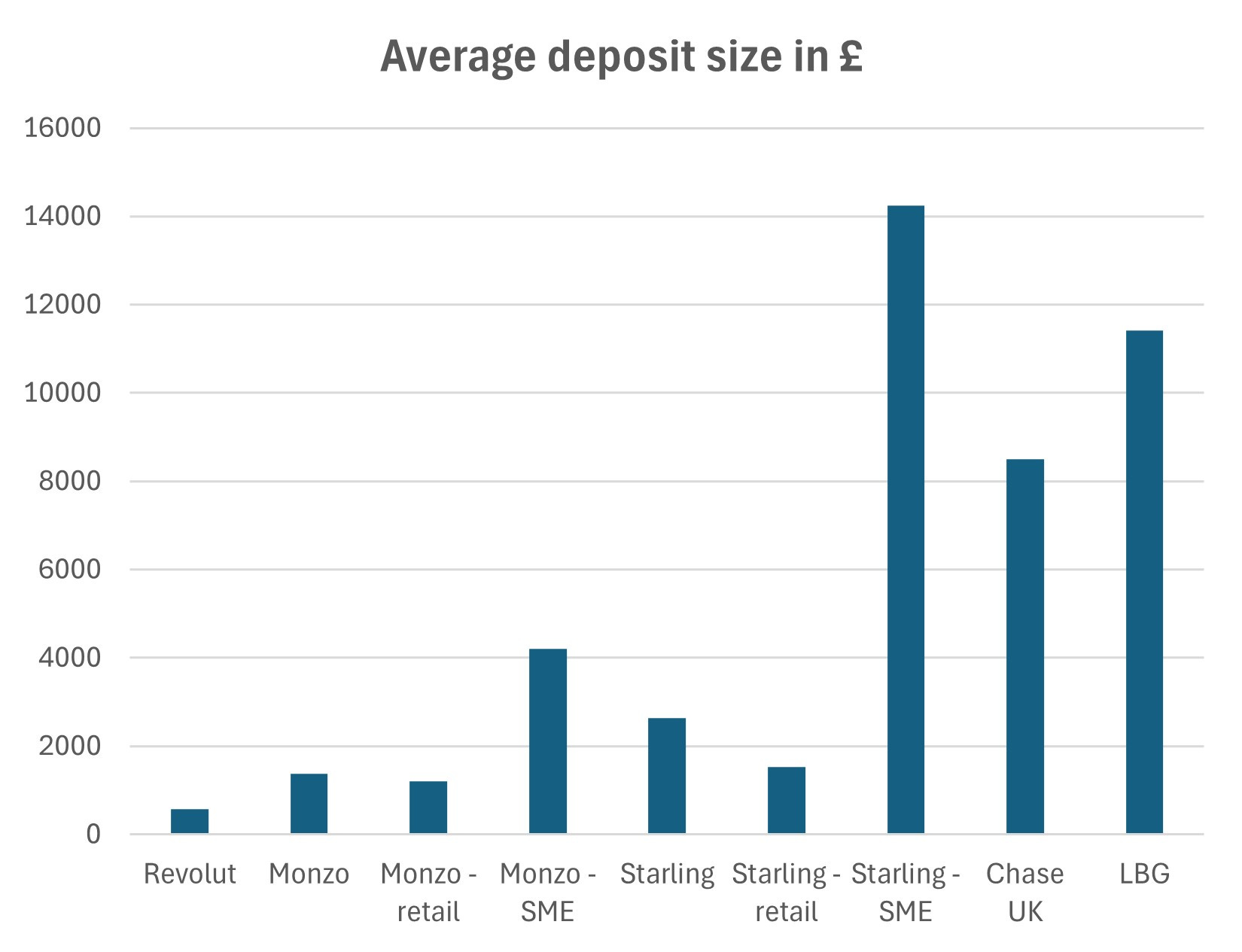

Despite 20% growth, the average deposit size at Monzo remains not just a fraction of the leading UK traditional bank Lloyds Banking Group but also a fraction of what new digital challenger Chase has in the UK. An average retail deposit size of a mere £1,200 when so many of these are already primary bank accounts makes me wonder if this is about timing (i.e., as customers growing older and more using Monzo as a primary account) or structurally a much less attractive income segment than the likes of Chase UK. Unlike Starling which saw its SME customer growth stall, Monzo saw tremendous growth of 205,000 to 625,000 SME customers but its average deposit sizes here are also extremely low and only grew by 10%.

Although Monzo’s retail and SME customer numbers grew significantly last year, two-thirds of its deposit growth came from its instant access savings accounts. The firm has 2.3 million of these accounts, which are more than half of all deposits (total deposits of £16.6 billion). Although this is a sensible strategy, just like we saw at Starling growing the deposit base this way can be costly. For some reason, neobanks always report headline revenues and growth before taking into consideration funding costs, while traditional banks have always looked at net interest income as part of revenues. Monzo’s gross interest income grew by 50% last year but net interest income grew by a slower 36% owing to the rise in funding costs (i.e., interest rates on savings accounts), in a similar fashion to what we saw from Starling.

By contrast, Revolut’s global customer balances grew by 66% last year to £30.2 billion with 75% of this customer deposits and the rest of this are in savings accounts with partners. Given the customer deposits are spread across 52 million customers it was virtually all in current accounts and they had to pay away very little in the Eurozone (where it already had a banking license).

The challenge for Monzo is that as it hit 12 million customers in the UK how further scope is there to grow this customer number? Lloyds Banking Group across its different retail brands, insurance, wealth management, and other services has 28 million customers in the UK. Barclays UK has 20 million customers. Lloyds also makes around ten times as much revenue in its retail bank than Monzo does. This shows the potential pie for Monzo. Not having a branch network is probably less of an issue today but the breadth of products those incumbents offer across loans, deposits, insurance, wealth, investment banking, and trading are of a different scale.

Monzo’s interest income from lending grew by a stellar 37% last year as its outstanding loans grew from £1.4 billion to £1.9 billion. The interest rates Monzo earns on this are high given it is all from unsecured lending and overdrafts. The associated credit loss expenses are down versus the prior year but still almost as high as the interest income from this lending. Expanding into lending is a different muscle to building a global scale in payments and given the type of lending, Monzo’s loan book is likely to be highly economically sensitive. The scale of Monzo’s lending is tiny when compared to not just the size but the breadth of offerings in the loan book of traditional banks.

Moreover, lending was only 9% of Monzo’s balance sheet at the end of March 2025. The vast majority of Monzo’s assets are merely money parked at the Bank of England, which is far more generous with the interest rates it provides to commercial banks than some other central banks. Monzo’s interest income from this cash at the Bank of England surged by 71% last year.

The additional challenge Monzo’s UK business faces is its reliance on net interest income. This has been 62-23% of net revenues for the last two years for Monzo, well below the circa 90% at Starling and OakNorth but well above the 25-27% of revenues at Revolut in the last two years.

The impact of recent and future Bank of England interest rate reductions will be a headwind for Monzo’s growth in the coming years. Around 40% of interest income will be protected by hedges at least in the near term.

Monzo is internally debating whether to list in its home market the UK where it has brand identity or the US where investors reward growth more. But US investors love recurring revenues, which as well as growth was a selling point for SaaS businesses. Monzo’s subscription revenues grew by 40% last year but at 7.5% of group revenue, they are still roughly half of Revolut’s proportion.

Monzo’s profitability has started to turn around after many years of losses. The adjusted net income was around £90-95 million last year. However, as the chart below illustrates this is still well short of all of its peers. Monzo’s staff costs (excluding share option revaluations) grew by 20% last year driven by a 20% increase in both customer and customer-facing headcount. But its other costs grew by 38%. Although most new customers come through word of mouth there was a huge increase in marketing spend as well as increased costs of managing customer accounts.

Revolut’s greater scale and faster growth are natural explanations for its superior operational leverage and overall profitability relative to Monzo. But here’s the thing. Revolut has more than four times as many customers as Monzo and is doing business in almost 50 countries while Monzo is only onshore in the UK currently and rolling out in Ireland. This illustrates the challenge for Monzo as it expands into the US and Europe in the coming years.

Does Monzo have a better mousetrap across European countries where Revolut, N26, Bunq, and others are expanding fast? Revolut is already in all these markets with 3-4 million customers in each major European country.

Revolut co-founder Nik Storonsky thinks having a banking license before launching is key in the US as it is a credit card-dominated market unlike Europe, which is a debit card-driven market. Storonsky believes that working with partner banks is not a viable option as it slows your ability to iterate products and can create regulatory bottlenecks. Monzo is taking the opposite approach going through partner banks in the US and without a banking license. It is hard to see what its differentiation will be in a market where there is also deep penetration of alternatives such as peer-to-peer networks VENMO and Block-owned Cash App.

Monzo was valued at £4.5 billion in a secondary offering last year a fraction of the $45 billion valuation that Revolut reached in a secondary offering last year. But the valuation multiple on last year’s earnings of £790m for Revolut and £90-95m for Monzo was broadly similar at 45-50x.

Revolut is reaching saturation in terms of customer numbers in many markets and it has risk and compliance infrastructure to build out, particularly given its new UK banking license. Monzo also has depressed margins that should offer greater upside - its net income margins (net income divided by net revenues) is only 40% of Revolut’s in the last financial year. However, Monzo is potentially at a bigger crossroads. Neobanks have struggled to attract decent average deposit sizes or become full-service lending banks in the UK. The obvious solution is international growth but unlike Revolut it hasn’t planted any acorns and growth may be costly in terms of money and time.