Are neobank's really tech or banking?

Nubank, Revolut, Monzo, Starling and OakNorth

In this first Substack of 2025, I look at:

What is fintech?

What do neobanks do and why are they special?

Are neobanks technology firms or banks?

Why does it matter if neobanks are tech firms or banks?

What is fintech?

My first exposure to technology in financial services in the late nineties was the hundreds of clunky Bloomberg terminals that filled the trading floor of CS First Boston’s Canary Wharf Office. I started working with the exchange sector 20 years ago and the industry was going through a revolution where there was a migration from the trading pits made famous in the movie Trading Places to a world of prices being disseminated on computers and new electronic trading firms. When I joined ICAP in 2012 the term fintech was not yet popular, but we were evangelical about our “technology assets” i.e. capital markets infrastructure like electronic trading platforms. Bloomberg was a frenemy of ours – a competitor, a customer, and a supplier. But there were lots of other fast-growing fintech assets such as the credit trading platform Marketaxess. There were so many such businesses that I had a schematic map in my office that had hundreds of “technology assets” on it big and small that fitted into our world of the trade life cycle. I also had a spreadsheet with our biggest clients and there were dozens of algorithmic trading firms like Citadel Securities.

A few years ago, the word fintech caught on, driven by venture capitalists. And it spread like wildfire across the traditional media and social media. But here’s the thing. I could see no mention of any of the businesses I had in my schematic map of capital markets tech.

To check the latest thinking the other day I asked ChatGPT what fintech is.

It talks about the integration of technology into financial services. It cites examples of mobile payments, digital banking, crypto, and robo-advisers.

There was no mention of the companies I had followed in capital markets infrastructure. If Bloomberg had been seeded by Sequoia and Tradeweb by Andreessen Horowitz would this whole space have been labelled fintech?

The reason I tell this story is that perception matters. If two businesses are the same but one is owned by a traditional bank and the other by a private unicorn fintech, would they be treated the same or treated differently?

What do neobanks do and why are they special?

ChatGPT says that “Neobanks are technology firms” but banks in a limited sense. It defines a neobank as a type of digital-only bank that operates entirely without physical branches. ChatGPT tells us a neobank is mobile-first, has fast account setup and instant transfers, leverages streamlined technology, is user-friendly, and offers financial tools. Most neobanks started in FX exchange and then moved into card payments, crypto, investing, and lending. Many of the features that ChatGPT gives as defining a neobank are now provided by traditional banks, but let’s look a little deeper:

1) Physical branch networks

Neobanks don’t have a branch network. A decade ago there was a large cost difference between traditional and neobanks owing to the physical branch networks of the former. But this is quickly disappearing. In the UK the number of bank branches has halved with over 6,000 bank branches closing.

a) LBG - The market leader Lloyds Banking Group (Lloyds, Halifax and Bank of Scotland) is down to around 1,000 branches which using an average cost per branch of £700,000 today (the FCA estimated that the average cost per branch in the UK was £590,000 in 2017 but with inflation it is likely to have risen) would be £700m. This is around 18% of LBG’s retail banking business profits.

b) Barclays - At the other end of the spectrum is Barclays, which has the smallest branch network out of the major UK banks, having closed 80% of its bank branches over the last decade. The cost of a Barclays branch network of around £200m comes to less than 6% of the profits it discloses for its UK retail and business banking unit. It is likely to be around 10% of the profits of its UK retail banking operations.

2) Mobile First

The traditional banks were woefully slow to respond to the smartphone era. In many ways, they have caught up since. As Akila Quinio wrote in Why fintech upstarts have failed to unseat UK banks the traditional bank’s mobile banking game has improved significantly. They offer many of the things that neobanks do like instant notifications on transactions. Account opening has also become easier albeit my best experience in recent years on account opening in terms of speed and ease was the neobank Chase UK. Moreover, for those looking for more from their mobile banking app, the neobanks still have advantages. Monzo and Starling are known for their budgeting and financial planning tools. Revolut is known for its easy-to-use multi-currency accounts, crypto, and together with Wise offering the best foreign currency transfer prices.

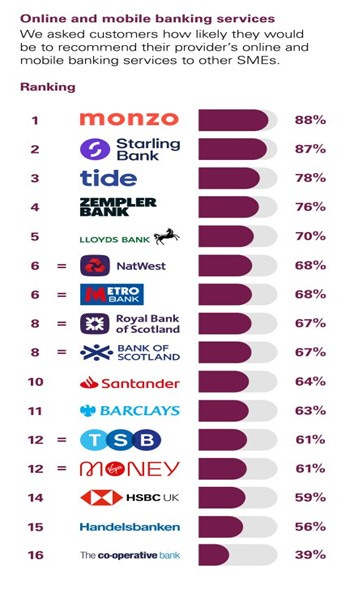

The superior customer satisfaction is illustrated by industry surveys. The UK government’s CMA (Competition and Markets Authority) commissions surveys every six months. The results have to be displayed by banks so that customers can see them. As they cover banks neither survey included Revolut, and it will be interesting to see how it does once it is included.

a) UK personal banking survey - The last Ipsos survey of personal current accounts included 17 banks and surveyed over 17, 000 people. Monzo, Starling, and Chase had the top 3 spots for both overall service quality and online/mobile banking.

b) UK business banking survey - In the area of UK SME banking the CMA appointed market research firm Bva-bdrc, who surveyed 19,200 people at 1,200 SME customers covering 16 banks.

3) Speed of transfers

a) Domestic payments are efficient in most countries - For most people, our everyday lives involve domestic payments and transfers. Real-time or near real-time central bank driven payment systems have spread like wildfire. In the UK individuals can move up to £25,000 and businesses up to £1m through this Faster Payments System launched in 2008. Other more recent real-time payment systems like UPI in India go beyond bank-to-bank transactions to wider use cases like merchant payments. The broad point is that the competitive advantage of neobanks is more limited in domestic payments.

b) Neobanks cheaper and faster in international payments - In international payments, neobanks have an advantage over traditional banks in terms of speed and cost. The roots of the likes of Revolut lie in offering a payment card that could be used abroad. Neobank leaders typically give you the market mid-price without egregious FX markups that traditional banks charge. The neobanks typically avoid the existing Swift messaging and global correspondent banking system. Without legacy IT and typically smaller volumes a neobank like Revolut does international transfers for its customers by collecting currency from the sender into Revolut’s own account in that country and paying out in a different currency in the recipient country through Revolut’s local bank account. Hence Revolut avoids moving money internationally for that specific transaction. If both sender and recipient have Revolut accounts this can happen on a peer-to-peer basis. Revolut had historically relied on a third-party Currencycloud (acquired by Visa) but has been taking these capabilities increasingly in-house. Revolut is still focused on smaller volumes though with Wise better for larger international transfers.

Wise follows a similar business model and many of Revolut’s competitors like Monzo, outsource cross-border payments to it. Although Monzo doesn’t have a wide international customer base like Revolut, the company tells me that its 11 million UK customers are heavily skewed towards young professionals many from international backgrounds that have FX needs. Starling, which has a much smaller customer base than Revolut and Monzo in the UK, and is more focused on UK SMEs, relies on the Swift system.

4) Streamlined technology

There is no doubt that neobanks benefit from having a fresh new technology stack with more tech-savvy management.

a) Neobank automation - Coming out of the gate as cloud-based and using a micro-services architecture allows them to respond quicker in terms of launching new features. Much has been written about Nubank’s extremely low cost to service customers vs legacy banks in Latin America for instance. There is also more automation of processes from customer onboarding, anti-money laundering, fraud detection, lending decisions, and customer service. Nubank was an early pioneer in using automation and technology to gradually extend credit lines on its credit cards. OakNorth in the UK has highlighted from its start the role of technology and some kind of AI in its lending decisions to its SME customers. 2025 is likely to see neobanks and fintech’s, follow the herd and pump up the noise around their use of automated self-learning software like AI agents.

b) The Klarna AI PR push - The most evangelical on using AI in the last year has been Sebastian Siemiatkowski, the CEO of Buy Now Pay Later firm Klarna. He has made a huge amount of noise about how AI has helped reduce headcount and costs for Klarna in marketing and customer service. Whether it was spin or not, both traditional outlets and social media lapped Klarna’s PR up with huge excitement. With Klarna’s cost base severely bloated and profitability challenged at a time it was looking to IPO, it is hard to know how much of this is better technology versus good old-fashioned cost-cutting. Klarna’s headcount has halved in recent years overall.

Customer service automation is an area where banks need to improve their game. But the evidence so far from those who have tried the Klarna chatbot is that it may have driven some cost savings, but it is not that far ahead of what some banks already have. Efi Pylarinou looked into the Klarna AI opportunity in the following piece https://efipm.medium.com/klarnas-genai-journey-a-case-study-using-the-ai-native-framework-0d741a193c8d and Gergely Orosz made the point that

“Automating L1 (Level 1) support is not that revolutionary and has been done previously on different systems. For example, if you have called phone support and experienced the automated “please press 1 for this, 2 for that” script; well, that was an early example of automating away L1 support,” in the piece

Klarna’s AI chatbot: how revolutionary is it, really? - The Pragmatic Engineer

Although Klarna is not directly a neobank, this is a good case study of perception versus reality in the fintech space!

5) Data-driven marketing approach

Leading neobanks have used a data-driven approach towards marketing, which has allowed them to have a lower cost to acquire customers, whether it is Nubank in Brazil or Revolut in Europe.

Nubank famously grew by word of mouth and built its highly profitable credit card platform using a tech and data-intensive approach slowly allowing its customers greater credit limits, tracking not just the credit histories of the customer but also other customers such as family and friends that may have been introducers through the referral program.

Revolut also had impressive results from its referral program, which includes incentives. It has ramped up its marketing spend significantly in recent years as it expands into new countries. Founder Nik Storonsky is keen to highlight the return on that spend and how virtually all of the spend is data-driven, and rather than brand advertising.

Are neobanks technology firms or banks?

I have outlined in the prior section many points that support the idea that neobanks are from Mars and traditional banks from Venus.

Neobanks are tech first and banking second.

But what will they look like when they are grown up?

To earn anywhere near the same economics from each customer as a traditional bank what does the business model look like and are technology-driven micro-services and customer acquisition more important than being an effective risk manager?

1) Becoming a tech company

There is a litany of word spaghetti and buzzwords associated with fintech and neobanks. There is embedded finance, which is supposed to be payments embedded into another product. Then there is the idea of a super-app i.e. the neobank mobile banking app will eventually aggregate all sorts of other services from taxis to food delivery. This may in the case in certain parts of Asia but a decade into European neobanks and even the VCs have gone quiet on this idea!

If a neobank does succeed in building a true super-app, in my mind it is a tech platform.

In the current AI hype cycle it may not feel like it but over the very long run economics matters as much as perception. The reason SaaS businesses were great is that they had sticky recurring revenues and low incremental operating and capital costs. A company making most of its money from net interest income is very different from that. To be fair to Revolut they are one of the few neobanks growing subscription revenues albeit from a low base.

2) Lessons from the Nubank experience

I have written in the past about how Nubank in Latin America is the gold standard of neobanks. It has delivered amazing growth and profitability, become the primary bank for more than 60% of its users, has a great app, has low customer acquisition costs, and is led by a visionary management team. Warren Buffet is a shareholder. My views on Nubank are very consensus. It is a darling of fintech followers, the VC crowd, and also generalist business commentators on social media.

a) The JP Morgan of Neobanks - Although Nubank hasn’t become a super-app in the WeChat sense (i.e. messaging, social media, payments, and a variety of e-commerce) it has a much higher customer penetration than other neobanks. The number of products (e.g. credit cards, payroll loans, insurance, wealth management) used by each Nubank customer has increased from 3 to 5 over the last 3 years. The average of 5 is almost twice the average number of products that customers of traditional Brazilian banks use.

Nubank customer numbers hit 110 million by the end of Q3 2024 with 20% growth year on year and 5% growth sequentially. 56% of all adults in Brazil are customers of Nubank. Moreover, in Q3 deposits grew 60% year on year, and lending even faster than this. This has driven an increase in net interest income on a constant currency basis by 63% year-on-year in Q3 2024.

b) A credit manager at heart - Here’s the thing. The core competency of all of these products, even under a data-driven approach with a high level of automation, is credit risk. Being an effective risk manager has been in the core DNA of the firm and that hasn’t changed. Net interest income is 65% of revenues and fees are only 35% of revenues.

Nubank’s recent results also highlight the importance of banking vs technology. There is still excitement about the potential to leverage its technology in newer markets like Columbia and Mexico. But revenue growth has slowed, net interest margins that expanded significantly over recent years have started to contract, interest rates that rose significantly in Brazil in recent years have started to fall and the deteriorating macro-economic outlook in Brazil is raising concerns about future loan losses.

After a long share price run-up with the boom in the Nasdaq and the rise in Brazilian interest rates, Nubank’s share price has now fallen more than 30% owing to these concerns in the last two months.

Nubank share price in $

3) UK Neobanks

The customer numbers and customer penetration of UK Neobanks are much lower than for Nubank. These neobanks have broadened out from just FX exchange but still sell far fewer products to their customers than traditional banks in their respective markets. The strongest of these is Revolut, which added more than 10 million customers in 2024 reaching a total of 50 million.

a) The Revolut Rocketship - Revolut recently outlined ambitions of growing to 100 million customers and revenues of $100 billion. This would be more than the largest US bank JPM Chase, which has 82 million retail customers and 6 million SME customers. But JPM Chase generates $70 billion of net revenues from these customers, which is 25x of what Revolut does. This illustrates the potential market wallet for neobanks that successfully manage the transition to selling more products to their customer base.

Revolut has many similarities with Nubank in terms of the pace of customer growth and the ability to scale its technology platform. Although it doesn’t have as many products as Nubank its geographical breadth is impressive with only 20% of customers from the UK and fast growth across a dozen countries in Europe. The latter partly explains its lower profitability, with operating margins in 2024 likely to be half of what Nubank achieves. Revolut’s revenue per head is also 60% of Nubank’s.

In 2024 Revolut is likely to generate revenues net of funding costs of around $3.5 billion and I would estimate that around 35% of its revenues is coming from net interest income. In this way, it is less of a bank than Nubank. Subscriptions were almost 15% of Revolut’s revenues in 2023 and Interchange from card payments and FX and trading including cryptocurrency are the main other categories. The challenge for Revolut will be that some of the upcoming levers of profitability - such as lending or getting access to higher interest rates from parking money at the Bank of England after receiving its UK banking license – are more banking than tech and even within banking relatively low multiple earnings streams.

b) The competitors - The other UK neobanks have even more dependence on net interest income and lending. Monzo is likely to have generated more than two-thirds of its revenues in 2024 from net interest income and for Starling and SME lender OakNorth this percentage is likely to be more than 90%. This is a far cry from the recurring revenues of a software business.

Banks have been trying to say they are tech companies for much of the last decade with limited success.

“We are a technology company” Marianne Lake JPM CFO Feb 2016

“We are a technology firm. We are platform” Lloyd Blankfein GS CEO early 2017

“We want to be a tech company with a banking license” Ralph Hamers ING CEO August 2017

Starling and OakNorth are both trying to sell their tech to other banks generating high returns and high valuation multiple software revenue streams. But so far, the number of clients and revenues from these sources has been negligible. Starling’s pivot from a planned geographical expansion into “Banking as a service” selling its tech platform to other banks is getting some headlines these days with management bullish and shareholders talking up the potential to create a decacorn business. It is early days but so far all they have announced are contracts with Salt, a Romanian digital bank, and AMP in Australia. Legacy vendors in the core banking engine space include the likes of FIS, Temenos, and Finastra but the cool sexy new cloud-native tech players are Mambu, Thought Machine, and 10x Technologies. The space is highly competitive and even these newer pure-play vendors are struggling to scale with high levels of cash burn.

c) Fraud and AML challenges – The neobanks have successfully followed the “move quickly and break things” approach of Silicon Valley. But how much of their faster product turnaround and lower customer acquisition costs are a function of lighter regulation?

Most of the neobanks got banking licenses many years ago and are regulated by the same people as banks. But here’s the thing. If the history of banking regulation teaches us anything it is that the scrutiny is related to the importance of an institution. As Revolut founder Nik Storonsky said recently, he had wished he had applied for a UK banking license when he had a small number of customers rather than 10 million in the UK. He noted how much easier the process would have been. The examples of major enforcement actions including fines for financial crime show that regulators can act with a lag of up to a decade after an event occurs.

Anti-money laundering and US sanctions list breaches have been an area where traditional banks have been fined tens of billions of dollars and had to increase their headcount and costs significantly. Neobank’s with a booming customer base are likely to face more scrutiny. Being tech first and banking second may sound good to neobank shareholders, but regulators will have little sympathy if automated checks and AI systems produce lots of false negatives and neobanks fail to police the money flowing through them adequately.

The UK regulator FCA fined Starling £29m last October for just such a failure. It said:

“Starling’s financial sanction screening controls were shockingly lax. It left the financial system wide open to criminals and those subject to sanctions. It compounded this by failing to properly comply with FCA requirements it had agreed to, which were put in place to lower the risk of Starling facilitating financial crime.”

Starling was also a great example of where the rubber meets the road on neobank technology replacing the humans and detailed processes of legacy banks. Starling found in 2023 that for the prior 6 years, its automated screening system for individuals on the sanction list had only been checking against part of the list!

Starling also suffered from the scandal around whether it properly assessed the Bounce Back loans it gave out during the Covid-19 period, which were underwritten by the UK government.

Other UK neobanks have also had their challenges over the years ranging from Revolut turning off its automated AML system for several months in 2018 to the ECB identifying shortcomings in Revolut’s financial crime control environment when it took over supervision of the bank in 2024. An example of how this can materially impact the growth of a neobank is German bank N26. German regulators severally capped the number of new customers N26 was able to onboard for many years, following major AML monitoring breaches. In December 2024 the Swedish regulator fined Klarna $46m after finding significant deficiencies in its money laundering and terrorist financing prevention systems. In the US, the high-profile failure of a VC backed fintech middleman Synapse led to large losses faced by customers.

The neobanks have also seen significantly more fraud complaints to the UK’s Financial Ombudsman Service (FOS) than traditional banks. Some of this is a function of their growth but leading UK banks like LBG still have customer numbers that are a multiple of Revolut and Monzo in the UK. The number of complaints in H1 2024 increased relative to the prior six-month period by 31% for Revolut to 2,888, 44% for Monzo to 1,864, and 9% for Starling to 378. For Revolut the year-on-year increase was 77%.

Why does it matter if neobanks are tech firms or banks?

Valuation multiples on bank stocks (8-12x PE albeit mostly valued on a price-to-book value basis) and tech stocks (25-40x PE) are very different. But of course, growth, profitability, and returns on equity within a sector matter as well. There is reason that JP Morgan and Morgan Stanley trade on a premium to other large Western banks and it is the combination of steady growth and far superior profitability and returns. Many banks in fast-growing emerging markets trade on a large premium to even JP Morgan, reflecting market expectations of superior growth, and in certain cases, they have even better profitability. One country where all the private sector banks trade on relatively high PE multiples of around 20x is India.

Following Nubank’s more than 30% share price decline its PE multiple is not that much higher than the leading emerging markets banks. Nubank trades on a price-to-earnings multiple of only 26x 2024E and 21x 2025E. This is hardly a tech sector multiple!

By contrast, the share price of leading FX transfer business Wise has risen almost 50% from its mid-2024 sell-off. It now trades at a slight premium to Nubank in terms of price-to-earnings multiples.

Nubank is likely cheap and will recover but UK neobank’s thinking about a stock market IPO even in the US shouldn’t assume that all revenue streams are worth the same. If I were a major shareholder, I would be telling them not just to focus on earnings growth but quality of earnings.

Nobody is going to put 25x PE on money that you park at the Bank of England earning attractive interest rates!

Thanks.

There probably is IMHO

Well researched and well written. Enjoyed reading this